KYCsphere’s digital account opening software offers a seamless customer self-service web portal where customers can submit account opening applications and subsequent service requests entirely online — without the need for branch visits. Banks and financial institutions are transforming how they acquire new customers through digital customer onboarding banking — replacing branch-based paper processes with a fully online, self-service account opening experience that meets all regulatory requirements while competing directly with the speed of fintech and neobank alternatives. As regulatory bodies including FinCEN, FATF, OFAC, and supervisors enforcing the Bank Secrecy Act increasingly accept and encourage digital KYC processes, financial institutions must deploy digital account opening solutions that balance frictionless customer experience with full BSA/AML compliance, FinCEN CDD Rule requirements, OFAC sanctions screening obligations, and FATF Recommendation 10 on customer due diligence.

KYCsphere’s digital account opening software offers a seamless customer self-service web portal where customers can open accounts and submit service requests entirely online. With AI-powered identity verification, automated document authentication, liveness detection, auto-population of existing customer data in relevant forms, and a robust back-office interface, the platform accelerates the digital onboarding process, reduces operational costs, and eliminates manual handoffs — while ensuring every regulatory compliance step mandated by FinCEN, FATF, OFAC, and local regulators is completed automatically before account activation.

Why Digital Account Opening Matters: Regulatory & Operational Context

The shift to digital account opening in banking is not just a convenience — it is rapidly becoming a regulatory and competitive necessity. FATF’s updated Guidance on Digital Identity (2020) explicitly recognises that reliable digital identity verification can be equal to or stronger than traditional face-to-face identification when properly implemented. FinCEN has similarly acknowledged through multiple advisories and rulings that BSA/AML obligations — including CIP requirements under Section 326 and CDD Rule requirements — can be met through digital and non-face-to-face channels, provided appropriate technology controls are in place. For institutions still relying on branch-based paper processes, the operational cost of manual account opening — staff time, data entry, error correction, and delayed activation — is the primary reason they lose new customers to competitors who have automated the same workflow end-to-end.

However, the digital onboarding process introduces unique challenges that purpose-built digital account opening solutions must address systematically:

- Remote identity verification without branch controls — Meeting BSA Section 326 CIP standards and FATF Recommendation 10 requirements for reliable identity verification without the physical document review that branch-based account opening uses as its primary control — and completing this fast enough that applicants convert rather than abandon

- Document authentication at scale — Detecting forgeries, altered documents, and synthetic identity fraud automatically across high application volumes — threats that are dramatically more prevalent in digital channels than in face-to-face settings, and that FinCEN has flagged in multiple advisories on identity-related suspicious activity

- Sanctions screening embedded in the flow — Real-time OFAC, UN, UK and EU Sanctions Screening embedded in the digital account opening workflow before account activation — not as a batch process after the customer has already been told their account is open

- Beneficial ownership for business account opening — Handling the additional complexity of business digital account opening — including UBO identification for corporate entities, trusts, and legal structures under FinCEN’s Beneficial Ownership Rule and the Corporate Transparency Act — within the same self-service portal used for retail customers, without a separate paper-based process for business accounts

- Risk-based compliance running invisibly — Applying appropriate CDD or EDD automatically based on each customer’s risk profile — so high-risk applicants receive additional scrutiny and standard applicants are approved immediately — without compliance steps slowing the customer experience or requiring manual analyst intervention at the point of application

KYCsphere’s digital account opening software addresses all of these challenges within a single, integrated platform — deployed as a cloud-based SaaS solution on Microsoft Azure with no capital expenditure, no lengthy IT project, and no developer involvement required to configure onboarding workflows.

See how KYCsphere delivers a fully digital account opening experience that meets BSA CIP requirements, embeds real-time OFAC screening, and applies risk-based compliance automatically — without slowing the customer down.

How KYCsphere’s Digital Account Opening Software Works

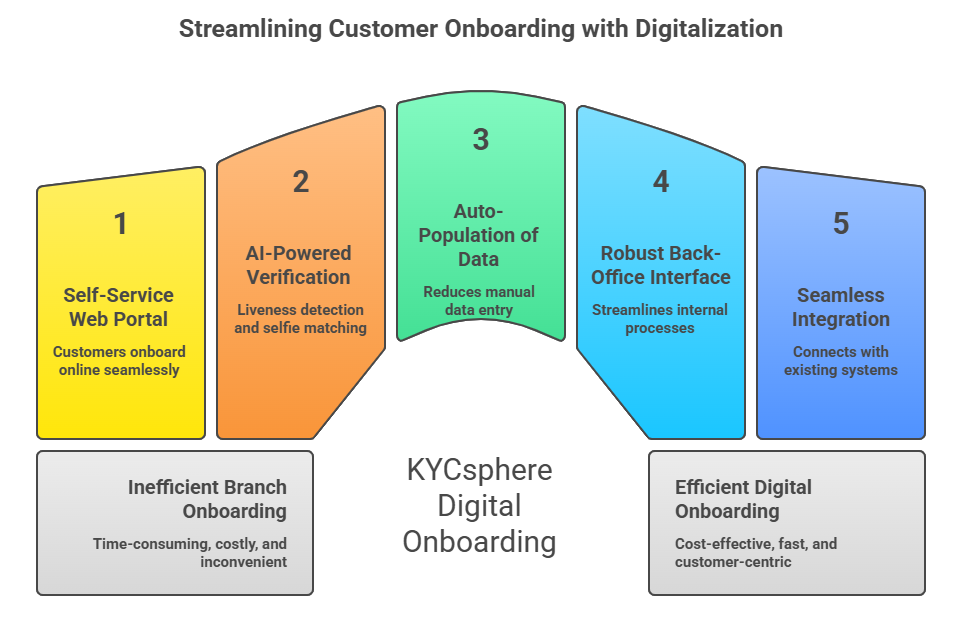

Self-Service Customer Portal

KYCsphere’s digital account opening portal is deployed as an integral part of your institution’s website, providing customers with a branded, consistent, and trustworthy account opening experience. The portal is the foundation of a digital customer onboarding strategy that removes the branch visit from the acquisition process entirely — replacing it with an adaptive, intelligent form flow that guides customers through application submission in minutes. Institutions prioritising intuitive experience for both customers and compliance analysts will find the portal surfaces only the fields, questions, and document requirements relevant to each specific customer type and product, so neither the customer nor the analyst is presented with irrelevant complexity. The portal supports:

- Retail and business account opening — Full control over account types, features, and additional services — tailored to meet the needs of individual retail customers and the more complex requirements of business account opening, including beneficial ownership questionnaires that adapt automatically to entity type under FinCEN’s CDD Rule and the Corporate Transparency Act. A single platform handling both retail and corporate customers eliminates the dual-process cost most institutions carry when they maintain separate workflows for each segment

- Subsequent service requests — Existing customers can submit additional product applications, account modifications, and service requests without branch visits — extending the self-service experience beyond initial account opening into ongoing relationship servicing, which compounds the operational savings from branch elimination across every subsequent customer interaction

- Auto-population of existing customer data — For returning customers, the portal pre-fills forms using existing profile data, reducing data entry burden and eliminating re-submission of documents that have not expired — improving completion rates, reducing abandonment, and delivering the measurable improvements in time-to-submit and data accuracy that operations teams track as primary digital account opening performance metrics

AI-Powered Identity Verification & Fraud Prevention

KYCsphere’s digital account opening software incorporates AI-powered identity verification that makes the compliance layer invisible to the customer while providing the institution with examination-grade evidence at every step. What separates a genuine digital account opening solution from a simple online application form is exactly this: customer data is not just collected — it is verified, authenticated, and cross-referenced in real time before the application proceeds:

- Liveness detection — Confirms the applicant is a real, live person — not a photograph, video replay, or AI-generated deepfake — catching synthetic identity fraud at the point of application, before an account is created

- Selfie-to-document matching — AI comparison of the applicant’s live selfie against the submitted identity document — verifying the applicant is the true document holder and automatically flagging impostor applications before any account access is granted

- Automated document authentication — Verifies government-issued IDs, address proofs, and corporate registration documents for authenticity — detecting forgeries, alterations, and inconsistencies between self-declared data and document-extracted information in real time, before the application proceeds

- Real-time sanctions and PEP screening — OFAC SDN List, UN Consolidated List, UK Sanctions List, EU Financial Sanctions List, and PEP and Adverse Media Screening embedded directly in the digital account opening workflow before account approval — with automated disposition documentation meeting FFIEC audit trail requirements, running entirely in the background without adding friction to the customer experience

Seamless Compliance Integration — Zero Data Re-Entry

The most powerful differentiator of KYCsphere’s digital account opening software is its straight-through processing (STP) architecture — data entered once by the customer flows automatically through every downstream system without any manual re-keying by bank staff. This is the architecture that makes digital account opening solutions for banks a genuine operational transformation rather than just a digital front end:

- KYCsphere Compliance Platform integration — All customer data captured through the portal automatically flows into compliance processing — Customer Onboarding, Sanctions Screening, PEP and Adverse Media Screening, Customer Risk Assessment and CDD/EDD — with zero manual data entry by compliance staff. The compliance team reviews exceptions, not every application

- Core banking system integration — Upon compliance approval, the verified and risk-assessed customer profile automatically flows into your core banking solution for account activation — eliminating duplicate data entry, reducing errors, and cutting time-to-account from days to minutes for straight-through-processing eligible customers

- Fully auditable digital trail — Every step — application submission, identity verification, sanctions screening, compliance approval, and account activation — is captured in a complete audit trail meeting FFIEC BSA/AML Examination Manual documentation expectations, FinCEN CIP record-keeping requirements, and BSA five-year retention obligations under 31 CFR § 1010.430

This straight-through processing approach means that from the customer’s online application to a fully active account in your core banking system, no manual intervention is required for eligible customers — transforming digital account opening from a cost centre into an efficient, compliant, revenue-generating process. Deployed on Microsoft Azure as a pay-as-you-go SaaS platform, KYCsphere scales with customer volume automatically, with no upfront capacity commitment and no long-term license obligation.

See how KYCsphere takes a customer from online application to fully activated account — with AI-powered identity verification, straight-through compliance processing, and zero manual data entry at every step.

What KYCsphere’s Digital Account Opening Software Delivers

- Branchless account opening with full regulatory compliance — Customers complete the entire account opening process online without a branch visit — meeting BSA CIP requirements, FinCEN CDD Rule obligations, FATF digital identity standards, and OFAC screening mandates in a fully digital workflow. For institutions measuring digital account opening performance, branch elimination alone reduces per-customer acquisition cost by 60–80% compared to manual in-branch workflows — with measurable improvements in completion rate and time-to-account as the primary operational KPIs.

- Dramatically reduced operational costs — By automating the entire digital onboarding process — from application capture through identity verification, compliance screening, and core banking integration — manual staff work is minimised, data entry errors are eliminated, and account activation time shrinks from days to minutes. Zero-data-re-entry, straight-through-processing architectures consistently deliver the highest ROI in the customer acquisition stack, reducing both cost per account opened and regulatory risk from manual data handling errors.

- AI-powered frictionless customer experience — An AI-powered, user-friendly dynamic interface ensures customers complete their digital account opening application with ease — boosting conversion rates and reducing abandonment. Intelligent form design adapts to customer type, product selection, risk profile, and jurisdiction, asking only relevant questions while capturing all required data. For frontline staff and compliance analysts, the back-office interface applies the same principle: surfacing only the review tasks, exception queues, and customer data relevant to each analyst’s role, so teams work faster and with fewer errors.

- Advanced fraud prevention at the digital front door — AI-powered verification — liveness detection, extracted selfie matching, automated document authentication, and real-time document-to-declared-data inconsistency detection — reduces identity fraud, synthetic identity fraud, and document forgery at the point of application. This directly addresses FinCEN’s advisory on identity-related suspicious activity and the growing deepfake threat flagged by FATF, protecting both the institution’s loss ratio and the customer’s identity.

- Cross-selling and revenue generation through data intelligence — By integrating the digital account opening platform with transactional data and existing customer profiles, institutions can identify cross-selling opportunities and deliver personalised product recommendations — loans, investment options, insurance, value-added services — directly within the portal. Product attachment rate, revenue per new account opened, and lifetime value by onboarding cohort all improve when cross-sell recommendations are presented at the moment of highest engagement: account activation.

- Seamless compliance platform and core banking integration — With seamless integration into KYCsphere’s Customer Onboarding, Sanctions Screening, PEP & Adverse Media Screening, Customer Risk Assessment, CDD/EDD and core banking solutions, all customer data flows automatically through compliance and account activation with zero manual data entry. This end-to-end integration makes KYCsphere the leading digital account opening solution for institutions that need compliance and onboarding to share a single data model — so customer data is consistent, compliant, and available across all systems from day one.

- Flexible configuration for retail and business customers — With full control over account types, features, products, and additional services, the platform handles retail account opening and the more complex requirements of business digital account opening — including UBO identification under FinCEN’s Beneficial Ownership Rule and the Corporate Transparency Act — all within the same portal without separate systems for each segment. For fast-growing fintechs and digital onboarding financial services providers, this flexibility is available on a pay-as-you-go basis without long-term licenses, scaling with customer volume automatically.

- Branded, trustworthy digital experience — As an integral part of your institution’s website, customers have a consistent, branded interaction throughout the entire digital account opening journey — enhancing credibility, trust, and digital banking adoption while the institution maintains full compliance visibility and control behind the scenes. Customers who complete account opening on your domain, within your brand environment, convert at significantly higher rates than those redirected to an unfamiliar third-party portal.

Request a demo and see how KYCsphere reduces per-customer acquisition costs, eliminates branch-based manual processes, and opens accounts in minutes — with full BSA/AML compliance built into every step of the digital journey.

Frequently Asked Questions

What is digital account opening software?

Digital account opening software automates the entire customer onboarding journey from initial application to full account activation — without branch visits, paper forms, or manual document processing. AI-powered self-service capabilities allow customers to apply on any device, submit identity documents digitally, complete biometric verification, and receive an account decision within minutes. Compliance controls — identity verification, sanctions screening, and risk assessment — run automatically in the background, so the customer experience is fast and frictionless while the institution meets its BSA/AML obligations at every step.

What are the best practices for customer onboarding in banking?

Customer onboarding best practices in banking centre on balancing compliance completeness with a frictionless customer experience. Key practices include: collecting only the data and documents required by regulation for each customer risk tier; using straight-through processing to auto-approve low-risk applicants without manual review; providing clear progress indicators and mobile-optimised interfaces to reduce drop-off rates; and routing higher-risk applicants to enhanced review automatically rather than applying the same manual process to every customer. Digital account opening platforms that integrate KYC verification, risk assessment, and AML screening in a single workflow deliver the highest completion rates while maintaining full regulatory compliance.

What is the customer onboarding journey in financial services?

The customer onboarding journey in financial services encompasses every step from initial application to a fully activated account relationship: application submission; identity document collection and verification; biometric liveness check; KYC risk assessment; sanctions and PEP screening; customer due diligence; account decisioning; and welcome communication with account access. Digital account opening software automates every step, with low-risk customers completing the journey in under five minutes via straight-through processing and higher-risk customers automatically routed for enhanced review with pre-populated risk profiles.

What are the best customer onboarding success metrics?

Key customer onboarding success metrics for financial institutions include: application completion rate — the percentage of started applications that result in an activated account; time-to-account — the average duration from application submission to account activation; straight-through processing rate — the percentage of applications approved without manual intervention; cost per onboarded customer — total compliance and operational cost divided by successfully onboarded customers; and false positive rate in KYC screening — the proportion of screening alerts that are not genuine risk indicators, which drives unnecessary review workload. Best-in-class digital account opening platforms benchmark all of these metrics and provide dashboards for compliance and operations teams.

How does digital account opening software support B2B customer onboarding?

B2B customer onboarding involves additional compliance requirements beyond individual customer verification: legal entity authentication, certificate of incorporation and constitutional document collection, and beneficial ownership identification for all persons holding 25% or more — under FinCEN’s Beneficial Ownership Rule. Best-in-class B2B onboarding platforms guide business applicants through structured UBO declaration workflows, verify entity identity against commercial registers, and screen all beneficial owners against sanctions, PEP, and adverse media databases automatically. The result is a compliant B2B onboarding process that can be completed digitally by the business customer rather than requiring branch visits or manual document submission.

What is straight-through processing in customer onboarding?

Straight-through processing (STP) in customer onboarding is the automatic approval and activation of a new customer account without any manual review or compliance intervention. STP is applied to applicants who pass all automated verification checks — identity authentication, sanctions and PEP screening, and risk scoring — within pre-defined thresholds, enabling account activation in minutes. Applicants that trigger manual review flags are routed to compliance queues automatically. STP rates are a key efficiency metric for digital account opening platforms: higher STP rates mean lower per-customer onboarding costs and faster customer activation, which directly impacts customer satisfaction and revenue.